CoreWeave IPO Filing Offers a Glimpse Inside

AI infrastructure service provider CoreWeave has filed an S1 prospectus with the U.S. Securities and Exchange Commission (SEC) in a step toward a future public offering.

The news comes as a range of similar GPU- and AI-software-as-a-service providers step up to lend AI infrastructure to the world’s largest companies as well as to enterprises seeking help with training and inferencing AI. These companies, including Crusoe, Lambda, Vultr and many others, are offering AI horsepower as a service alternative to AI infrastructure offered by hyperscalers AWS, Microsoft, IBM, Google, and Oracle.

According to Bloomberg, CoreWeave could raise roughly $4 billion on an anticipated valuation of more than $35 billion in its anticipated IPO.

Revenue Growth and Losses

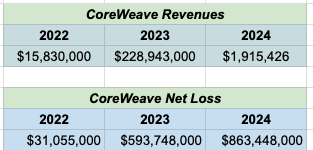

Over the past three years, CoreWeave revenues have skyrocketed, growing 737% between 2023 and 2024, as companies such as Microsoft have been quick to adopt its services to train and process large language models (LLMs). At the same time, the costs of procuring GPUs from investor NVIDIA and building 32 datacenters throughout the U.S. and parts of Europe has also risen, leading to yearly net losses and an overall corporate deficit of $1.5 billion as of December 31, 2024.

Source: CoreWeave S1

Big TAM, Many Risks

CoreWeave views its opportunity in the market as massive. In its S1 filing, it quotes Bloomberg Intelligence as estimating the market size for AI infrastructure related to its services at $399 billion by 2028, representing a 38% CAGR from 2023 through 2028.

At the same time, CoreWeave cites many risks to its potential success. Among these are the risks for supply-chain bottlenecks and rising costs related to the tariffs and regulations imposed by the current U.S. presidential administration. Also cited are risks related to the company’s datacenters, including power shortages and losses as well as potential security breaches.

Other concerns include customer concentration. Microsoft accounted for 62% of CoreWeave revenues in 2024, and a second customer accounted for another 15%, bringing CoreWeave’s dependence on two customers for 77% of its revenue last year. If demand from Microsoft lessens, that will affect CoreWeave’s financials. And word that Microsoft may be shuttering many of its AI datacenter plans may indicate a rationalization of AI demand.

CoreWeave also has acknowledged a weakness in its ability to track its financial reporting, a shortcoming it relates in detail in its filing, along with the steps it’s taking to remedy the situation. Of course, the company needs to get its financial reporting act together quickly in order to conform to the strictures of public company reporting.

A Profile of CoreWeave’s Infrastructure

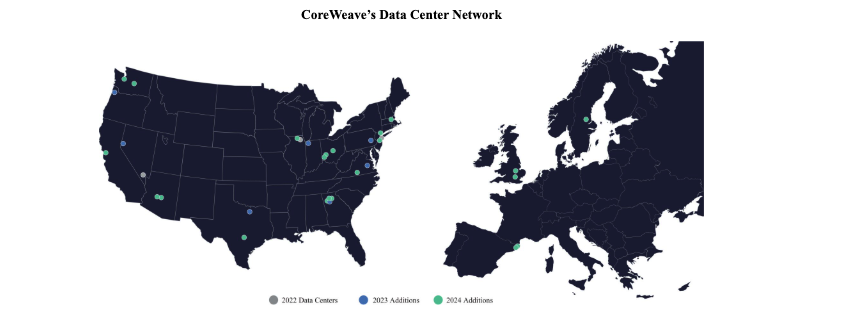

Apart from concerns, the S1 reveals a great deal about the size and nature of CoreWeave’s AI infrastructure, which in turn reflects on key trends in the AI space. Here’s a look at some key figures, all applicable as of December 31, 2024:

Datacenters: 32 in total, including 28 in 15 U.S. states, along with 2 in the U.K., one in Sweden, and one in Spain. Total power represented is 360 MW.

Source: CoreWeave S1

Cooling: Liquid cooling throughout.

GPUs: 250,000, all NVIDIA, including the GB200 NVL72 (the Blackwell GPUs).

Networking: InfiniBand between clusters, comprising 3,200 Gbps of non-blocking GPU interconnect. Blackwell deployments tap NVLink switches between GPUs and CPUs.

Storage: Object storage was announced last November, and taps a proprietary Local Object Transport Accelerator, which caches data locally onto GPU nodes. Microservices architecture supports a range of third-party storage backend resources.

Software resources. Included is CoreWeave Kubernetes Service (CKS); provisions for virtual private clouds and bare metal; a range of Application Software Services including Slurm on Kubernetes integration (SUNK); and Inference Optimization and Services.

Futuriom Take: CoreWeave’s S1 filing is a mixture of strengths and significant weaknesses. Customer concentration and a heavy dependance on the AI boom mark the highest risk factors for investors.